YahooFinance/Quandl data downloader

complete list of free datasets provided by Quandl check https://www.quandl.com/search?filters=%5B%22Free%22%5DExamples:(a) Yahoo Finance disp('Request historical YTD Bitcoin price and plot Close, High and

Provides functions for getting data from both data sources as well as helper utility functions

This archive contains functions for downloading daily stock price information from both Google and Yahoo! Finance as well as helpful utility functions. It furthermore contains a (basic but decent

discrete-time and continuous-time processes for finance, theory and empirical examples

, subordination. To walk through the code and for a thorough description, refer to A. Meucci (2009), "Review of Discrete and Continuous Processes in Finance - Theory and Applications", available at

The script downloads 10 years of stock data from Yahoo Finance.

Downloads 10 years worth of daily stock data from yahoo finance. The open, high, low prices are adjusted based on the adjClose field.The output is saved in csv format in the directory specified by

This code connect to Yahoo finance and download live continuous call and put option prices

Download current and future option prices from yahoo finance. This code goes toyahoo finance page and get quotes for a given stocks and strike prices. No toolboxes is needed just an access to the

Chapter-by-Chapter MATLAB codes related to the book "Computational Finance. MATLAB oriented modeling"

Friendly GUI for download historical stocks prices from Yahoo Finance

This file is a friendly GUI for download historical stock prices from Yahoo Finance using the file "hist-stock_data.m" created by Josiah Renfree. You need to download Josiah Renfree's file so you can

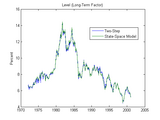

Stochastic State-Space Modeling in Finance

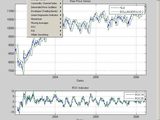

Forecasting the FTSE 100 with high-frequency data: A comparison of realized measures

Version 1.3.0.0

Oleg KomarovMy dissertation for the MSc in Finance & Economics from Warwick Business School

View and add transactions to portfolios on Google Finance. A Google account will be required.

Attached are two very simple functions demonstrating how you can view and add transactions to portfolios on Google Finance from Matlab.Update: I can only get these functions to work on Matlab 2008b

Contains Matlab function to gather stock's data from Yahoo Finance.

An easy to use class to download, display, and plot stock information from Yahoo finance.

Use this simple, self-contained class definition to obtain quotes and historical data from Yahoo finance.f = stock('f','5y','d);creates a stock object with a current quote and five year history of

Realtime trading demo & presentation, presented at NYC Computational Finance Conference 23 May 2013

These are the files used for my presentation "Realtime Trading with MATLAB", at the MATLAB Computational Finance Conference in New York on May 23, 2013, and updated for the MATLAB Computational

Implementation for Head-And-Shoulder (Lo et al., 2000, Journal of Finance) with simulated data

This prototype shows a reduced approach, how to implement an automated pattern recognition algorithm for the Head-And-Shoulders pattern (Lo et al., 2000, Journal of Finance) in MATLAB.Lo et al. (2000

Retrieves historical stock data from Yahoo Finance by parsing html pages instead of .csv download.

This is an updated function to retrieve historical data from Yahoo Finance.Apparently they changed things around May 2017 and previous versions of these types of functions stopped working. This is a

Implementation of the Paper Arbitrage-Free SVI volatility surfaces in Quantitative Finance 14:1

Simple Econometrics and Computational finance Laboratory Toolbox for MATLAB 7.x

Simple Econometrics and Computational finance Laboratory Toolbox for MATLAB 7.x

Retrieve historical stock data from Yahoo! Finance

The function obtains quote from google finance into command line variable

Couldn't find a working version of quote retriever so built my own.usage:>> gequote = get_gf_quote('ge','detailed')Obtaining Google finance quote for ge...gequote = quote: 12.8600

GUI for viewing various simple technical analysis indicators of a time series

gathers historical stock information from Google Finance.

This program gathers the historical stock information from the Google Finance website. The data is gathered in a struct containing the date, open, high, low, close and volumes for the stock. The

Download daily data and profile data from Yahoo Finance Japan and plot candle chart. Yahooファイナンスから日足データとプロファイルデータをダウンロードして、ローソク足チャートを表示します

Japanese.Yahooファイナンスからデータ取得して表示します。日足データ:移動平均を計算し、ローソク足チャートを表示できます。プロファイルデータ:次のデータを取得して、ファンダメンタルズ解析に利用できます。市場区分、業種、時価総額、発行株式数、配当利回り、1株配当、PER、PBR、EPS、BPS、最低購入代金、年初来高値、年初来安値、出来高、売買代金、信用買残、信用売残、信用倍率、上場年月日These programs acquire data from Yahoo Finance Japan and show figure.Daily data: Calculate the moving average and plot candle chartProfile data: Acquire following data to analyze fundamentals. Market

Learn how to use MATLAB and R together to tackle your computational needs

This submission contains files from the “MATLAB for R Users in Computational Finance” webinar, highlighting the interconnectivity between MATLAB and R, and some of the differences between the MATLAB

Performs various time series analysis operations

- Tool that downloads financial time series data from finance.yahoo.com and performs various time series analysis operations- Documentation of functions to follow with the next release- Further

Free historical data downloader from Yahoo! FInance with symbol lists: stocks, ETFs, Indices, Forex. FOR PERSONAL USE ONLY.

Free historical data downloader from Yahoo! FInance with symbol lists: stocks, ETFs, Indices, Forex. FOR PERSONAL USE ONLY.

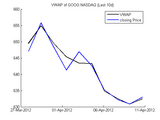

Retrieves the VWAP from intra-daily data of Google Finance

This package allows you to [1] retrieve intra-daily stock price data from Google Finance, [2] calculate the VWAP at the end of each trading day and [3] transform intra-daily data to a daily

A beginners tool for analysing time varying coefficients within regression analysis.

Output set of stock prices from yahoo finance as a matrix with header and dates into excel

Version 1.4.0.0

Haidar HaidarOutput historical stock prices for a basket of stocks and given period as a matrix with header

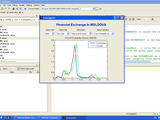

Display in the GUI evolution of the Finance in Moldova

Code to download option chain data from Google finance.

I wrote this after existing Matlab code out on the web for downloading stock option chain data from Yahoo Finance started failing in the fall of 2014. This code download the json file from Google

These are the supporting MATLAB files for the MathWorks webinar of the same name.

or academics in finance whose focus is risk management, credit structuring, quantitative analysis, or asset valuation. Familiarity with MATLAB is helpful, but not required.

These codes are all created for my Honours Project in Advanced Matematics of Finance.

This function obtains the current stock price of the input tickers.

This function obtains the current stock price and other stock info of the input tickers (up to 200 tickers) from Google Finance with the undocumented Google Stock API.

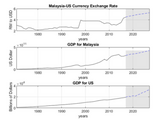

Models VAR using GDP for Malaysia, GDP for U.S. and Malaysia/U.S. Foreign Exchange Rate

modelProduct Focus :MATLABDataFeed Toolbox (Computational Finance Suite)Econometric Toolbox (Computational Finance Suite)[Note : Not advocating any particular strategy, factors or methodology]

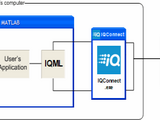

Matlab connector to IQFeed

function getHistoricalIntraDayStockPrice obtains intraday stock price from Google.

alternatives.https://stackoverflow.com/questions/46070126/google-finance-json-stock-quote-stopped-workinghttps://stackoverflow.com/questions/51658401/google-finance-api-address-has-changedFor the adventurous folks, I recommend giving Quantopian (python) or Quantconnect (python, c#) a try. Both platforms provide free intraday data as long as you are doing analysis/trading within their

Used to retrieve historical stock data for a user-specified date range

This program uses the Yahoo! Finance website to download and sort historical stock prices or dividend data for a user-specified time period. The user can either supply the program with individual

Function to smooth call option prices and implied volatilities free of static arbitrage.

The function is an implementation of the method proposed in Fengler, M. (2009). Arbitrage-Free Smoothing of the Implied Volatility Surface. Quantitative Finance, 9:4, 417-428.The method uses

Implementation of Option Pricing Transform Methods

The CFH toolbox is a collection of characteristic function transform methods in finance that can be used for example for pricing American/European style options in affine jump diffusion models such

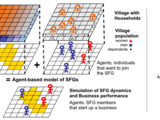

Replication package of the article "Bifurcations in business profitability: An agent-based simulation of homophily in self-financing groups"

MatLab codes that allow to simulate a stochastic micro-verse of nano-finance groups in an artificial village. The codes simulates the impact of social capital on the business joint ventures started

Kalman Filter is applied to estimate the parameters of CIR interest rate model.

Corresponds to the paper "estimating and testing exponential-affine term structure models by kalman filter" published by Review of Quantitative Finance and Accounting in 1999.

Access and download data from the Quandl database from inside the MATLAB console.

Quandl.com is an aggregator of over 3 million economic, finance, and sociological time series datasets. This function allows you to pull data directly from Quandl into MATLAB for analysis, from the

It contains necessary functions or tools required for option pricing and prediction

Code and Examples for "Developing Robust MATLAB Code"

errors, for example. In this session at the MATLAB Computational Finance Conference 2018, we learned about relevant advanced MATLAB software development capabilities, including error handling

Generate Matlab table for ticker(s) queried through Alphavantage

Estimation of zero yield curve from coupon bond prices by Nelson-Siegel or Svensson model.

error measures.More details: Kladivko Kamil (2010). The Czech Treasury Yield Curve from 1999 to the Present, Czech Journal of Economics and Finance, 60(4): 307-335

Get HTML-table data into MATLAB via urlread and without builtin browser

Version 1.0.0.0

Sven KoernerBased on getTableFromWeb with a little more functionality for bring in table data from web to MATLAB

; % Table with the travelinformation data out_table = getTableFromWeb_mod(url_string, nr_table)% Finance example % run getTableDataScript to see, which table is number 7 (Valuation Measures)url_string

Extension of Datafeed Toolbox's Yahoo object, allowing real-time data to be fetched

YAHOORT Extends the Datafeed Toolbox's YAHOO object, allowing real-time data to be fetched from Yahoo's Premium Finance service.Requirements:- Datafeed Toolbox license- Yahoo account subscribed to

Pricing Guaranteed Minimum Withdrawal Benefit

Highlights include:• Integrating data sources• Valuing and creating a variable annuity product• Application development and deploymentThis webinar is relevant to practitioners or academics in finance

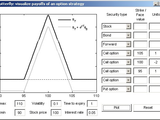

(via an interactive GUI)

Function BUTTERFLY (named after the strategy shown on the screenshot) aims to help students and instructors of finance visualize payoffs of simple option strategies. The function allows constructing

it use Machine Learning in MATLAB to predict the buying-decision of Stock by using real life data.

Handling downloaded data from Yahoo Finance using the timetable objectSelecting features based on domain knowledgeMachine Learning ModelingAutomate to re-train new model to incorproate new updated data for

Monte Carlo Schemes for advanced models and pricing of derivatives

Illustrates methods from Chapter 7 of the Wiley Finance series title Financial Modelling by Joerg Kienitz and Daniel Wetterau. eWe cover Monte Carlo simulation by considering path discretisation for

Provide the Next $VIX Expiry Date, Given a Single Calendar Date

is included that (unlike those in the finance toolbox) retains the query date if already a biz date but otherwise gives the immediate next or previous biz date. This can be used for other purposes but

Convex versus Concave Management, CPPI, OBPI, portfolio insurance, etc.

Copula functions written for Master Thesis.

Functions written in 2007 for Master Thesis: "Simulating dependent random variables using copulas. Applications to Finance and Insurance". Functions include MVCOPRND - multivariate copula generator

This function gets the list of symbols for stocks from indices and/or sectors.

This program gets the stock symbols of a user-defined index (NASDAQ, NYSE, AMEX, OTCBB, LSE) and/or sector. The data is retrieved from http://www.eoddata.com/ and from Yahoo Finance.For example: -

Optimize portfolio weights for a weighted linear combination of Sortino ratio, Sharpe ratio, total return, downside risk, SD, & max drawdown

falls among other randomly generated portfolios on the highest-weighted dimensions. The function was designed using data from Yahoo Finance (https://finance.yahoo.com/) but should work with other data

Get stock option chains.

Pulls stock option chains from finance.yahoo.com with Yahoo! Query Language.--Updates09JUL2014 1) now supports miniOption, implemented by G (matlab central author # 379241).09JUL2014 2) now supports

Estimates the parameters of the two factor CIR model on the UK German, and US term structures.

Term Structure: Estimates and Tests from a Kalman Filter Model,” The Journal of Real Estate Finance and Economics 27, no. 2 (2003): 143-172.etc.Please comment or leave suggestions.thanks Bill, 27493

You can also select a web site from the following list

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)

Asia Pacific

- Australia (English)

- India (English)

- New Zealand (English)

- 中国

- 日本Japanese (日本語)

- 한국Korean (한국어)